That mobile loan apps are in high demand in Kenya has never been in doubt. However, just like with anything and everything that is in demand in this country, mobile lending has attracted quite a number of players some that have a very good reputation with their users and excellent services and others that are as shady as shady gets. The latter’s struggles are either in fulfilling the expectations of their users or, generally, providing a desirable user experience in-app. No one wants to be stuck on the registration page of a mobile money lending application yet all they needed was to quickly sign up and request a small boost as they struggle through January.

A lot can be said about best practices around taking credit and whatnot but this is not the place for such discussions. Whether the monies requested via these apps is used well or misused is a different ball game altogether. What I know is that as a big believer in technology and how it can make our lives better, mobile lending apps are a god-send. Instead of having to borrow small amounts from your friends and risking relationships that have taken you years to build, you can just turn to an app and be sorted in a matter of minutes.

The crux of the matter is that thanks to Kenya’s leaps and advancements in mobile money, it is now, more than ever before, quite easy to access credit facilities on the go without having to queue all afternoon long and scratching your head as to where you’re going to fish 3-months pay slips from just to get a small loan to see you to the end of the month.

In the course of regularly writing about Android finance apps over the last one year, I have come across quite a number of mobile loan apps that Kenyans are using and which, if Google Play Store data is anything to go by, are quite popular.

Fortunately or unfortunately, I have, over the last two years, tried, tested and actually used for quite some time, only three mobile lending solutions which will be the subject of this article as I know just about everything there is to know about them as far as user experience permits. These are Safaricom’s M-Shwari, Inventure’s Tala and Branch International’s Branch.

The beauty of being an Android device user is such that thanks to Android devices being available at various price points, from dirt cheap to insanely expensive, it is the platform of choice for many people around the world. Kenya is not an exception.

As such, most developers, moreso of services looking to deepen financial inclusion, tend to focus on the platform at the expense of others like Apple’s iOS. While an argument can be made about the disparities that exist between iPhone users and Android device users and their varying needs, the bottomline is there are some perks of sticking with your buggy droid, after all.

Of the three services, only Safaricom’s M-Shwari is available cross-platform, thanks to the service being an offshoot of M-Pesa, Safaricom’s renowned mobile money platform.

Branch

My first run-in with Branch was probably one of those situations where many find themselves in and opt for such services. It was the Boxing Day (December 26th) of 2015. I was at home and flat out broke. I hadn’t gone out the previous day (Christmas) opting, instead, for a silent Christmas at home doing nothing but watching TV. It was one of those times in my past when I was dead broke. My graduation, just the previous week, had seen me opt for a rather muted celebration because money was a problem and my mother’s health was at its worst. As is usually the norm, Boxing Day means lots of Premier League action and there was no way I was going to stay at home feeling sorry for myself just because I was broke yet it’s known that there is a direct correlation between my level of happiness and seeing my favourite Reds doing their thing at Old Trafford. So I decided to test an app I had kept on my phone for a while but had never used: Branch. That would mark the start of a long relationship with Branch.

My story is not the most ideal and, definitely, this is not how to go about this whole mobile loans thing but hey, I am not your financial advisor.

Branch relies on Facebook user data (and, I think, past M-Pesa transaction data from SMS) to map out the risks associated with lending to a user. How they exactly do this, I have no idea since I am not privy to the inner workings of the application and the system it relies on. What I know for sure is that to use Branch, one needs two things: a Facebook account and a Safaricom SIM that is registered on the M-Pesa platform. Just those two things. Well, and internet access since, unlike M-Shwari, apps like Branch need a constant line of communication between your device and Branch’s servers/systems.

Thanks to that Facebook integration, there’s not much in the form of interrogation that a user has to put up with. Just sign up and you will be presented with an initial assessment as to whether you qualify for your first loan or not. One places a request for a loan from the app. Before doing so, they are given a detailed breakdown of the final amount they will be expected to pay once the loan matures which is typically a month (30 days). Subsequent loan approvals are dependent on how one repays any previous loans advanced to them via the app.

What I have gathered about Branch from my 2 years of using the service is that it is one you can rely on. The only time I was ever denied a loan (I had requested for just Kshs 1,000 in January 2016 just over a week after I had repaid my very first loan), Branch sent me a text message a few days later informing me that it had been as a result of a system error after an upgrade their systems had undergone and that it shouldn’t ever happen again. True to their word, that has never happened again. I’ve only needed to keep my end of the bargain: pay my loans on time.

The only time I was late in repaying my loan, late October to early November 2016, I incurred a penalty of Kshs 566 on top of the Kshs 1,132 that I was supposed to pay for a Kshs 1,000 loan that had been advanced to me in late September. On top of that, my loan limit was lowered as a result. I was late on my repayment for a whole 16 days and the consequences were dire. If you do the math, that’s too steep a penalty on top of already high interest rates. I know they justify these crazy rates because of the risk involved (there’s no collateral of any sort) but still… That should give you a picture of what you are getting in to when considering Branch and other such apps to bail you out. The next time (and last time) I defaulted on my loan was at the start of February 2017 but I paid it 5 days later after my salary hit the account (yes, my broke self used to live from hand to mouth).

From my experience, loan approvals are instant. That hasn’t always been the case, though. It’s just that their systems have gotten better with time. In the early days, I used to wait for hours. Today, it’s instantaneous.

Reliability aside, I like how responsive Branch’s customer service team is. The customer service team is reachable directly from the app through the “Customer Care” option on the app’s slide-out menu. While they’re not always at hand to respond to queries (the last time I used the option, it took almost an hour to get a response), at least it’s much better than having to go to another app (email or the dialer app to make a call) for help.

Sometime in 2016, the app received a huge update which made it more appealing and usable. The end result is the app you can find today on the Play Store which is easy to navigate and the most detailed of those that this article focuses on. Besides building in the customer care section, it’s also easy for users to view their transaction history.

The only problem I have with the Branch app is the lack of a PIN code or a safeguard of any sort. When you open the Branch app you are directly taken to your “My Loan” page where you are presented with a loan offer or, in the event that you had already taken a loan, with a status (days remaining to your next repayment, the amount itself, the interest etc). This is quite risky. Should one’s device fall in the wrong hands, anyone with malicious intent can use the opportunity to do whatever they want – request for a loan or simply get to know information they were not supposed to know. This is a serious omission and I have no idea why it has taken this long for the feature to make its way to the app. Tala has it and M-Shwari is, well, M-Shwari.

Branch seems to have learnt a thing or two from the likes of Uber since it has a referral program where users can invite their friends and in return, receive Kshs 500 when those invited repay their first loan.

Tala

Tala’s previous name, Mkopo Rahisi, Kiswahili for “easy loan” pretty much sums up what one can expect from the app.

Since unlike Branch it does not rely on a third-party service to access user data, one has to sweat blood and tears in terms of the information one has to give out. Your employment status, salary, M-Pesa SMSs… Stuff that will make you think twice. Uncomfortable.

Like Branch, Tala is limited to Safaricom M-Pesa users since the service uses M-Pesa to disburse loans as well as accept repayments.

Once one has managed to go through Tala’s lengthy onboarding process, they get a status bar on the app that shows them where they fall in the pecking order. It is this “status” that determines one’s loan limit. The highest status is “Gold”. Users with a “Gold” status can, theoretically, borrow as much as Kshs 50,000 from Tala. I say theoretically because just recently the upper limit for Tala loans has been lowered to just Kshs 20,000 before being raised again to Kshs 30,000. Either the defaulting rate is quite high or Tala is also, like the rest of us, having its January moments.

Like Branch, Tala’s loan limits are purely informed by one’s repayment history. There is no magic involved. The more one pays on time the closer they get to their “Gold” status.

While I understand and appreciate the need for simplicity, Tala’s app is too simple and mean on the details. Besides the open invitation to take a loan, providing status information and showing users the band they are in as far as borrowing limits go, there’s not much else on the app. No slideout menu offering users their transaction history.

While the Tala app does have an option for customers to get in touch with the customer service team, it is buried deep under a barrage of FAQs. I understand the need to have customers messaging the customer service team only if their concerns are not already addressed in the FAQs but…

The one thing I like about Tala is that every time they send you a loan, they also make sure to send you an email informing you of the same complete with a breakdown of the total amount owed and the due date. In the event you ever default, email reminders will be sent to you in addition to the usual SMS alerts.

Loan approvals are also instant.

Like Branch, Tala’s interest rates are also quite high.

Tala also has a referral system in place but users only get Kshs 200 for inviting their friends to use the app, lower than Branch’s Kshs 500.

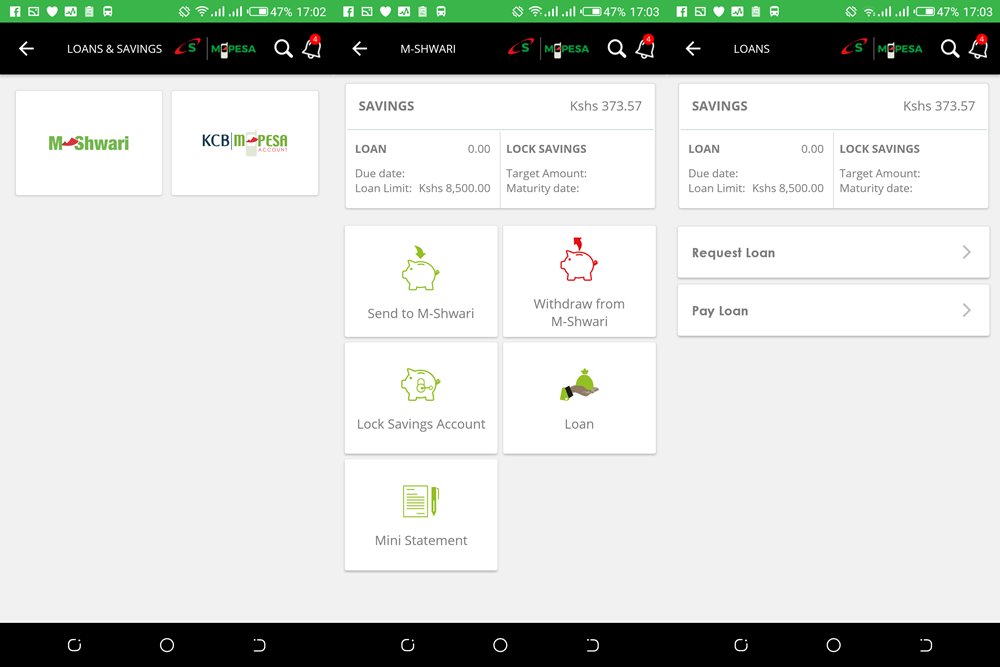

M-Shwari

If there was ever to be a mother of all mobile lending services in the country then Safaricom’s M-Shwari is a strong contender for the title. The service recently celebrated its fifth anniversary and currently boasts of over 21 million users across the country.

Of all the services highlighted in this article, M-Shwari is the easiest to go with. The barrier for entry is pretty low. Just a Safaricom SIM that is registered for M-Pesa is needed. Nothing else is required. From the M-Pesa menu on every device’s SIM toolkit, anyone can enrol for M-Shwari. Easy. No need for internet access or even a smartphone so as to download an app. However, they will need to have been on the M-Pesa platform for some time, at least 90 days the last time I checked (correct me if I got this wrong) before being in a position to borrow from the service for the first time.

Being simple and easy to access for the masses, while good, has meant that M-Shwari has trailed the competition and their flashy mobile apps for quite some time now. However, with its recent inclusion in the Safaricom mobile app, that gap has been closed and it’s all down to the service offerings.

As far as service goes, M-Shwari is definitely up there thanks to its 7.5% “service fee” which is charged on all loans disbursed (and doubled in the event one defaults). Tala and Branch’s interest fees vary depending on the loan amount (the higher the loan, the lower the interest rate). Of course, how low these rates are is all relative, they are actually exorbitant when you look at them from an annual interest rate perspective. Usurious.

If it matters, M-Shwari has a leg up in all this mobile loan business because it is the child of the service that everyone competing against it uses: M-Pesa. As a result, users don’t pay any additional costs when repaying their M-Shwari loans. Tala and Branch users have to part with additional charges in the form of M-Pesa transaction fees since the two services use a Pay Bill number.

However, M-Shwari’s main undoing is that it takes forever to raise the credit limits of its users.

When it launched, it was promised that loan limits would be based on one’s M-Pesa transaction habits as well as usage of the service itself (M-Shwari). The service, in this case, is not M-Shwari the loan service but rather its savings option. Remember, M-Shwari is a savings and credit facility and, in its early days, a lot of emphasis was placed on the savings aspect of M-Shwari more than the lending bit. With over Kshs 230 billion being disbursed over the last 5 years in the form of mobile loans to its users, M-Shwari is now known to many for its credit feature. Though we’ve been promised that things will get better, it’s still murky as hell. The last time I had my loan limit increased was, I think, two years ago? Desperate to grow their loan limits, some users I know even resorted to depositing money and withdrawing it from their M-Shwari savings every now and then hoping to fool the system with their “high volume” transactions and frequency. That’s crazy given how smooth the process is with Tala and Branch.

Like Tala and Branch, approval for M-Shwari loans is instant.

I just have one gripe: since I started repaying my M-Shwari loans via the app, I don’t get any confirmation text messages. It’s happened all the time and across all the phones I frequently use.

Advantages of these mobile loan apps/services (Tala, Branch and M-Shwari)

- Reliable.

- Loan approvals are instant.

- One can do partial payments (even though only M-Shwari explicitly encourages this).

- You don’t get to deal with people and their emotions. Things are algorithm-driven. No relationships are at risk of being ruined. No use of pawns for security/collateral.

Disadvantages of these mobile loan apps/services (Tala, Branch and M-Shwari)

- High interest rates. They range from 7.5% (M-Shwari’s “service fee”) all the way to 15% for Branch and Tala. Crazy. Per month!

- High penalties for defaulting. Like being charged twice the interest/”service fee”. Again, crazy.

- While the loan approval process appears streamlined and quite instantaneous, there is a price to pay: all that data you are giving away! Are you comfortable giving out your employment history, your M-Pesa transaction SMSs and other data to third parties?

- At this point in time, it is not possible to have someone else chip in to pay your mobile loan for you from their mobile money account. At least as far as I know (I am open to correction on this matter).

- I get it, we can’t use any of these apps on multiple devices because, security, but I am still gutted that I usually have to go through the whole process of activating the apps (Branch and Tala) on any new device I am using.

Note: I started writing this article in January 2018. By the time you’re reading it (after publication in mid-April 2018), quite a number of things may have changed though not so drastic as to affect the fundamental approach and the intent to just analyze the three services. I cannot guarantee 100% accurate information, as such. Reader discretion is advised.